Every public orthopedic and spine product supplier has now reported sales results for 2021, the year after COVID and, roughly, the 60th year since the advent of modern orthopedic and spine surgery.

2021 Ortho and Spine Review, 2022-2025 Outlook

4 min read Premium comments

#hipproductsales#kneeproductsales#spineproductsales#surgicalrobotsales

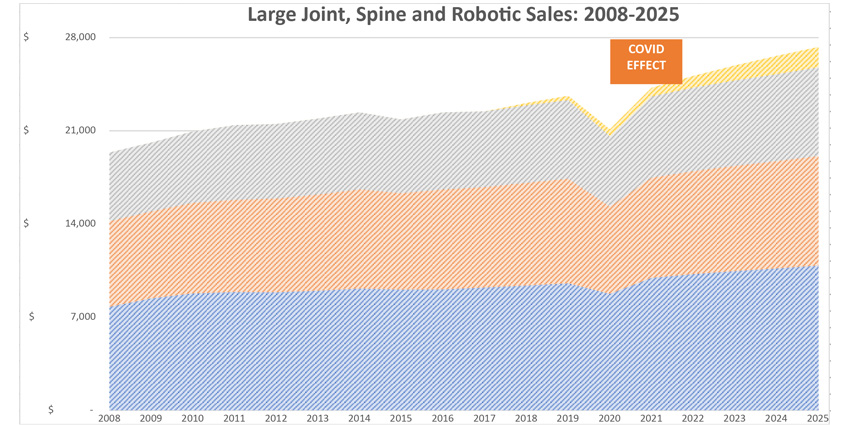

Aggregate sales of knee, hip, spine, and robotic products rose 14.8% in 2021 to reach $24.2 billion (does not include trauma or extremity sales). For those analysts on Wall Street who forecast orthopedic and spine revenues and earnings, the reports were an upside surprise.

The year before, 2020, COVID effectively shut down roughly two-thirds of the industry for several weeks and the industry reported $21.1 billion in sales, down 10.7% from 2019.

Aggregate Market Share Changes

The largest supplier of orthopedic and spine products in the world is Zimmer Biomet.

In 2021, the companies who gained the most knee, hip, spine, and robotics market share in the aggregate were:

Large Joint Sales and Market Share Changes

Global sales of hip and knee products reached $13.6 billion in 2021, up 15.1% from $11.8 billion reported for 2020. Because of COVID, overall sales of hip and knee products fell 14% in 2020 from 2019 levels. The largest global supplier of hip and knee products is Zimmer Biomet with annual knee and hip sales of $4.7 billion.

The company which gained the most market share in 2021 was Stryker Corporation.

Spine Sales and Market Share Changes

Global sales of spinal products reached $9.9 billion in 2021, up 13.7% from $8.7 billion reported in 2020. Because of COVID, overall sales of spinal products fell 8% in 2020 from 2019 levels. The largest global supplier of spinal products is Medtronic Spine with annual spinal product sales of $3.1 billion.

The company which gained the most market share in 2021 was Alphatec Spine.

Knee Sales and Market Share Changes

Global sales of knee products reached $7.5 billion in 2021, up 14.9% from $6.5 billion reported in 2020. Because of COVID, overall sales of knee products fell 17% in 2020 from 2019 levels. The largest global supplier of knee products is Zimmer Biomet with annual knee product sales of $2.7 billion.

The company which gained the most market share in 2021 was Stryker Corporation.

Hip Sales and Market Share Changes

Hip Sales and Market Share Changes

Global sales of hip products reached $6.1 billion in 2021, up 15.2% from $5.3 billion reported in 2020. Because of COVID, overall sales of hip products fell 10.4% in 2020 from 2019 levels. The largest global supplier of hip products is Zimmer Biomet with annual hip product sales of $2.0 billion.

The company which gained the most market share in 2021 was Stryker Corporation.

Robotics (Non-Spine) Sales and Market Share Changes

Robotics (Non-Spine) Sales and Market Share Changes

Global sales of robotic assist products reached $667 million in 2021, up 27% from $526 million reported in 2020. In 2020, despite COVID, overall sales of spinal products rose 58.9% (off a low base) from 2019 levels. The largest global supplier of non-spine robotic assist devices is Stryker Corporation with annual robotics product sales of an estimated $307 million.

The company which gained the most market share in 2021 was JNJ (DePuy) which is due to the initial commercialization of the VELYS system.

Underlying Orthopedic and Spine Sales Trends

Underlying Orthopedic and Spine Sales Trends

This is a low-single-digit revenue growth industry. On average, since 2005, the business of selling spine, knee, and hip products has grown 1.69% per year. In effect, it is growing a little slower than underlying population growth.

Here’s the data.

Forecast 2022-2025

For 2022, the rebound from COVID will continue to deliver, we think, above average rates of sales growth across all the orthopedic and spine categories resulting in a 3.5-4.0% range. Robotics, augmented reality and virtual reality tools will contribute to overall growth rates and keep them above the core, 1.88% annual rate of growth for implants and instruments.

Source: RRY Publications LLC

Finally, it’s worth noting that the historic core growth rate of 1.88% is substantially below where Wall Street’s analysts are forecasting. On average, Wall Street is expecting annual revenues to rise between 4 and 5% annually between 2021 and 2025. That’s highly unlikely, we think. While digital technologies will raise company growth rates, in the aggregate, they won’t likely move overall growth rates much beyond 3% annually.

How to Get Your Own Copy of the Ortho and Spine Sales Dataset

The entire dataset from which this article is based is available to paid OTW Subscribers. To obtain the dataset: email yoko@ryortho.com. This dataset includes the following.

- Hip Product Sales

- 2008 – 2021

- Global sales

- S. Sales

- OUS Sales

- Company Sales:

- Biomet

- Johnson & Johnson (DePuy)

- Other Large Joint

- Smith & Nephew

- Stryker Corporation

- Zimmer Biomet

- Market Share analysis

- Average Annual Growth Rate analysis

- Underlying population growth rates

- 2008 – 2021

- Knee Product Sales

-

- Global sales

- S. Sales

- OUS Sales

- Company Sales:

- Biomet

- Johnson & Johnson (DePuy)

- Other Large Joint

- Smith & Nephew

- Stryker Corporation

- Zimmer Biomet

-

- Spine Product Sales

-

- Global sales

- S. Sales

- OUS Sales

- Company Sales:

- Alphatec Spine

- Globus Medical

- Johnson & Johnson (DePuy / Synthes)

- Medtronic Spine

- NuVasive

- Orthofix Medical

- Other Spine Suppliers

- SeaSpine

- Stryker Spine

- Zimmer Biomet (ZimVie)

-

- Joint Arthroplasty Robotic Assist Sales

-

- Global sales

- S. Sales

- OUS Sales

- Company Sales:

- Johnson & Johnson (DePuy)

- Other Spine Suppliers

- SeaSpine

- Stryker Spine

- Zimmer Biomet (ZimVie)

-

- Industry sales forecast 2021-2025

- Hip Sales

- Knee Sales

- Spine Sales

- Robotic Device Sales

Tables Source: Company Reports, Wall Street Analyst Reports, SEC Filings

Author

React:

Discussion

This is a fascinating development. In my practice we've seen similar outcomes with the revised protocol. The key differentiator seems to be patient selection criteria. Has anyone else noticed the correlation with BMI thresholds?

Great point. I'd push back slightly on the conclusion, the sample size in the cited study is too small to draw population-level inferences. That said, the directional signal is compelling and worth a larger RCT.

We implemented a similar approach last year. Early results are promising but we're still gathering 12-month follow-up data. Happy to share our protocol if anyone is interested.

Join the conversation

Orthopedic professionals are discussing this. Sign in and upgrade to read every comment and add your voice.