Signs of the times. Semi-conductor chips are the new oil. The “Age of Information” continues its inevitable march across industries. Autonomous trucks. Q-codes instead of menus. And smart, really smart, implants and robotic assist devices in surgery. Software and ever more powerful semi-conductor chips, in other words, are creating new delivery and supplier eco-systems all around us.

10 Ways Software-Based Tech Will Transform Ortho and Spine

6 min read Premium comments

#futureofmedicine#orthopedicsandspine#surgicalrobots

In Orthopaedics and Spine four powerful trends seem poised to transform patient intervention up and down the continuum of care and, in the process, upend business models and redefine product design.

The four trends are:

- The Internet of Things – where implants, devices, OR tables and, even OR walls will become intelligent things with the ability to collect, process and communicate information.

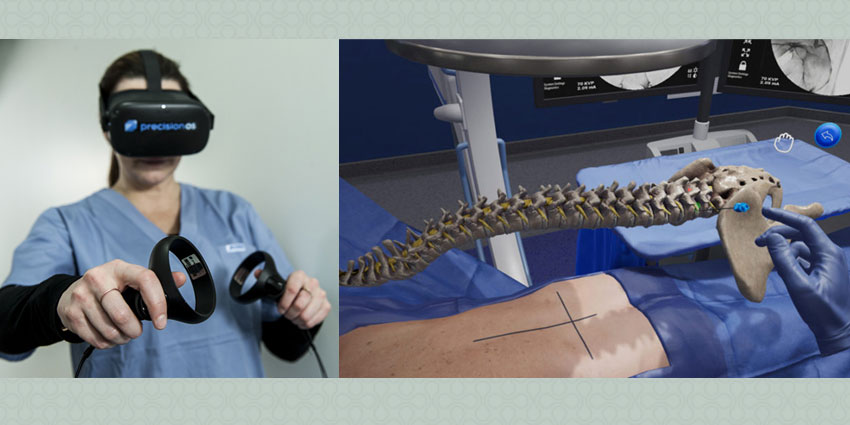

- Robotics – which have been in manufacturing since the 1980s now deliver enhanced dexterity, intelligence, sensing and communicating capabilities to the surgeon. Robotic assist devices expand human capabilities.

- Artificial Intelligence (AI) – we are entering a new age of AI where software will increasingly simulate how physician brains learn, reason, understand and make decisions.

- Computational Power – all of the above are possible because computational power continues to grow at exponential rates. If you have not seen Intel’s latest ad, you should. Intel is now producing quantum processors in Oregon and doing system-level engineering that targets production-level quantum computing within ten years.

A new generation of companies and surgeon leaders is riding these trends. They represent a clear divergence from the change agents of twenty years ago. They don’t make the implant or teach the procedure; they make the implant or procedure better (also cheaper and more accurate).

I will be delivering a major address on the subject of emerging technologies in Orthopaedics and Spine at the 2021 North American Spine Society (NASS) annual meeting in Boston on Wednesday, September 29, at 2pm in the Exhibit Hall.

Twenty-five years ago, as a Wall Street analyst, I helped to direct significant levels of investment into companies like Sofamor Danek, Spine Tech, DJO, Perclose, Arterial Vascular Solutions and a couple dozen more. Back in the day, my firm and its investor clients put approximately $100 million into those companies, which at the end of five years was worth more than $600 million.

Now is the time for investors—whether purchasing equity or investing time to learn and understand these technologies—to get involved.

Joining me on the podium at NASS will be three legendary investors in disruptive Orthopaedic and Spine technologies—Anthony, Mark and John Viscogliosi.

Please reserve time on your calendar to attend this major address. It will be one of the most important talks of the year. You won’t want to miss it.

10 Ways Software-Based Technologies Will Transform Orthopaedics and Spine

In 2004, the Boston Red Sox won their first World Series in 86 years. Facebook launched its social media platform to a few thousand Boston and Ivy League college students and Google went public at $85 per share.

Most people don’t remember that Google struggled in its initial public offering. Underwriters had to cut the IPO price from between $108 and $135 to between $85 and $95. On that first nail-biting day of trading, Google’s stock opened at the low end of the expected range before rising 18% to close at $100 per share. Investors who bought $100,000 of Google’s IPO stock…and held on…now have an investment worth $4.3 million—a 24.8% average annual return on investment (ROI).

Since 2004, Facebook has grown from a few thousand college students to 3 billion users. Google now provides search services to half the planet (4 billion people).

Software combined with computing power is transformational.

Here are ten ways the treatment of Orthopaedic and Spine patients will change because of a new generation of powerful software algorithms and computing power.

- All implants will be smart. Everything implanted in the human body will eventually have sensors, computing and communication capabilities. The information will include basic implant ID as well as real-time data about biologic processes surrounding the implant and any catastrophic failure.

- All operating room equipment will be networked. A new networked, intelligent framework will emerge linking and exchanging data between the equipment in the OR, the hospital/clinic, individual healthcare providers, payors and possibly regulatory agencies and manufacturers. This connectivity of smart equipment will lead to a ubiquitous understanding of surgeon behavior and patient outcomes. It may also lead to the end of the electronic health record.

- Surgery will be cheaper, faster, more reliable. The new framework of intelligent operating room equipment will result in improved surgical efficiencies, higher productivity, reduced costs, and increased hospital/ambulatory surgery center (ASC) profitability. It may also speed up implant and instrument innovation cycles. Applying the Internet of Things to surgery is a strategy to reduce surgeon variability and improve the overall Orthopaedic and Spine service model.

- Robotics will change the limitations of what surgeons can do. Robotics have reached a tipping point where scale and functionality are improving at exponential rates. Not only will robotics deliver super-human levels of dexterity, sensing, intelligence but also steadiness and reliability.

- Artificial Intelligence will drive a cognitive revolution in Orthopaedics and Spine. Over the last decade significant increases in data and computational power have driven a revolution in artificial intelligence capabilities. AI will be a key disruptor to both the treatment of patients and the business models of hospitals, clinics but interestingly, also manufacturers and regulators.

- AI will be embedded in payor systems, hospital software, diagnostic and image equipment. As AI becomes more universal, new knowledge will be created at an explosive rate, supplementing—occasionally supplanting—surgeon decision making by leveraging deep data domains. The hospital service model will change. Manufacturers will become information providers. Implants will become commoditized hardware where the value add will be its level of intelligence. A good analogy is the automobile industry. The frame of the “family” car is evolving into commoditized hardware where the value proposition is embedded intelligence—leading ultimately to an autonomous, on-call vehicle.

- Digital delivery of orthopaedic and spine services will increase. Teledoc was just the beginning. Digital labor has the ability, actually, to increase collaboration between service providers by leveraging AI and process robotics to augment or automate certain tasks. Combined with human ingenuity, digital labor will improve the ability to read digital images, infer causes, context, progression or sources of disease, reason through probabilistic outcomes and learn from experience.

- Cybersecurity will get smarter and more prevalent. Smart, interconnected systems will have the ability to collect and analyze surgeon and patient behavioral, diagnostic and treatment data—“learning” surgeon and patient patterns, inclinations and preferences. That will fundamentally change the concept of security and require ever more robust and tailored cyber security systems.

- Competition will come from new players. We are currently in the dis-intermediation stage of the digital revolution in Orthopaedics and Spine. The surgeon “champion” is already a casualty of these changes. Platform companies (large healthcare provider systems and large, integrated Orthopaedics and Spine companies, large payors) will face a different type of competitor from big tech and emerging software start-up companies. Reflect on how a small software company named Uber transformed the sleepy taxicab industry. Big tech (Amazon, Google) and emerging start-ups will use software to reduce complexity and create new value propositions in Orthopaedics and Spine service delivery.

- Access to capital will favor software driven innovation. Access to capital is a limiting factor to innovation. Investors have had the benefit of watching software dis-intermediate industries and create new wealth over the past quarter century. Today’s capital markets are favoring companies that bring software based solutions that replace the middlemen, cut costs, raise efficiencies, and provide outsized returns on investment (ROI).

To summarize, Orthopaedics and Spine are at a watershed moment. A new generation of wealth producing companies, innovative surgeon and knowledge leaders are upon us. We have not seen this level of orthopaedic innovation since the Charnley hip, the Steffee Plate, BMP-2, prodisc® or MIS surgery—when the future of Orthopaedics and Spine seemed wide open to creative innovation.

Join me on September 29 at the North American Spine Society annual meeting in Boston, 2pm in the Exhibit Hall auditorium for a major talk about emerging technologies in Orthopaedics and Spine. RSVP here.

Author

React:

Discussion

This is a fascinating development. In my practice we've seen similar outcomes with the revised protocol. The key differentiator seems to be patient selection criteria. Has anyone else noticed the correlation with BMI thresholds?

Great point. I'd push back slightly on the conclusion, the sample size in the cited study is too small to draw population-level inferences. That said, the directional signal is compelling and worth a larger RCT.

We implemented a similar approach last year. Early results are promising but we're still gathering 12-month follow-up data. Happy to share our protocol if anyone is interested.

Join the conversation

Orthopedic professionals are discussing this. Sign in and upgrade to read every comment and add your voice.